The Most Brutal Single-Month Plunge in 43 Years, Gold's Every Top Looks Like This

In January this year, gold reached a historic high of $5,589. In less than two months, the price dropped to around $4,100, experiencing a peak-to-trough decline of 26.6%, marking the most severe monthly drop in 43 years.

The direct transmission chain of this sharp drop is not complex. Into the third week of the US-Iran conflict, the Strait of Hormuz was blocked, causing oil prices to rise by over 40% since the outbreak of the conflict. According to data from the US Bureau of Labor Statistics, the February CPI reached a new high since last year, coupled with the lagging effects of high tariffs, fueling market concerns about inflation. In the latest Summary of Economic Projections (SEP), the Federal Reserve narrowed its interest rate cut expectations for 2026 to only once, essentially announcing the end of the recent easing cycle. The US Dollar Index broke through the 100 mark, exerting comprehensive pressure on precious metals and base metal prices.

However, the macro narrative is only half the story. According to Finance Magnates analysis, the technical breakdown of the 50-day moving average (around $4,978) triggered a concentrated stampede of "crowded long positions," with cascading stop-loss and margin call orders being activated. Gold rose from $2,600 to over $5,000 within 12 months, with a large amount of leveraged funds accumulating in long positions. When the escalation of the conflict drove up oil prices instead of gold prices, these crowded positions became the first chips to be sold off.

The price drop itself is not the story. The story is: this "geopolitical shock driving inflation, concentrated unwinding of leveraged trades" script has played out at least three times in the past 46 years.

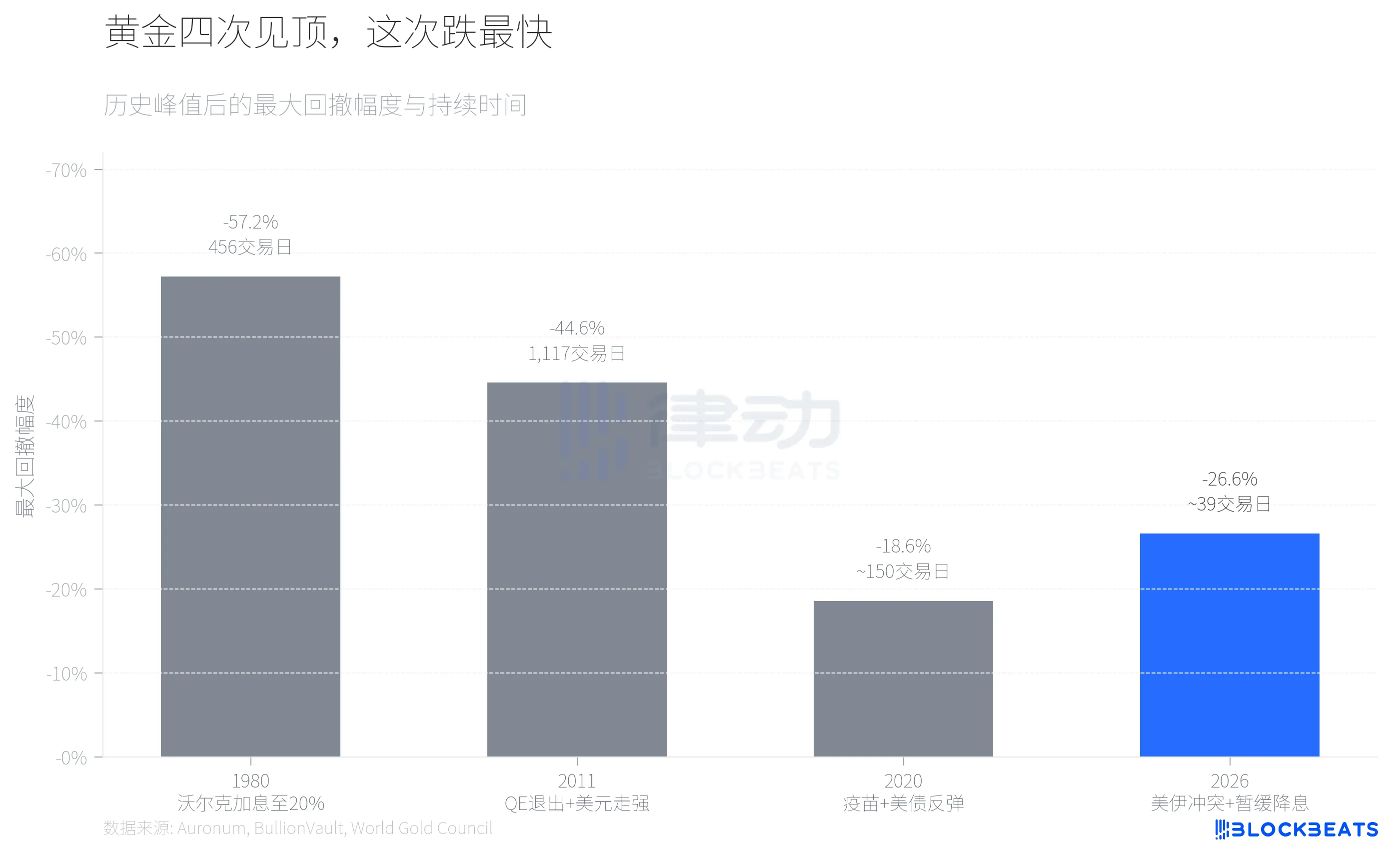

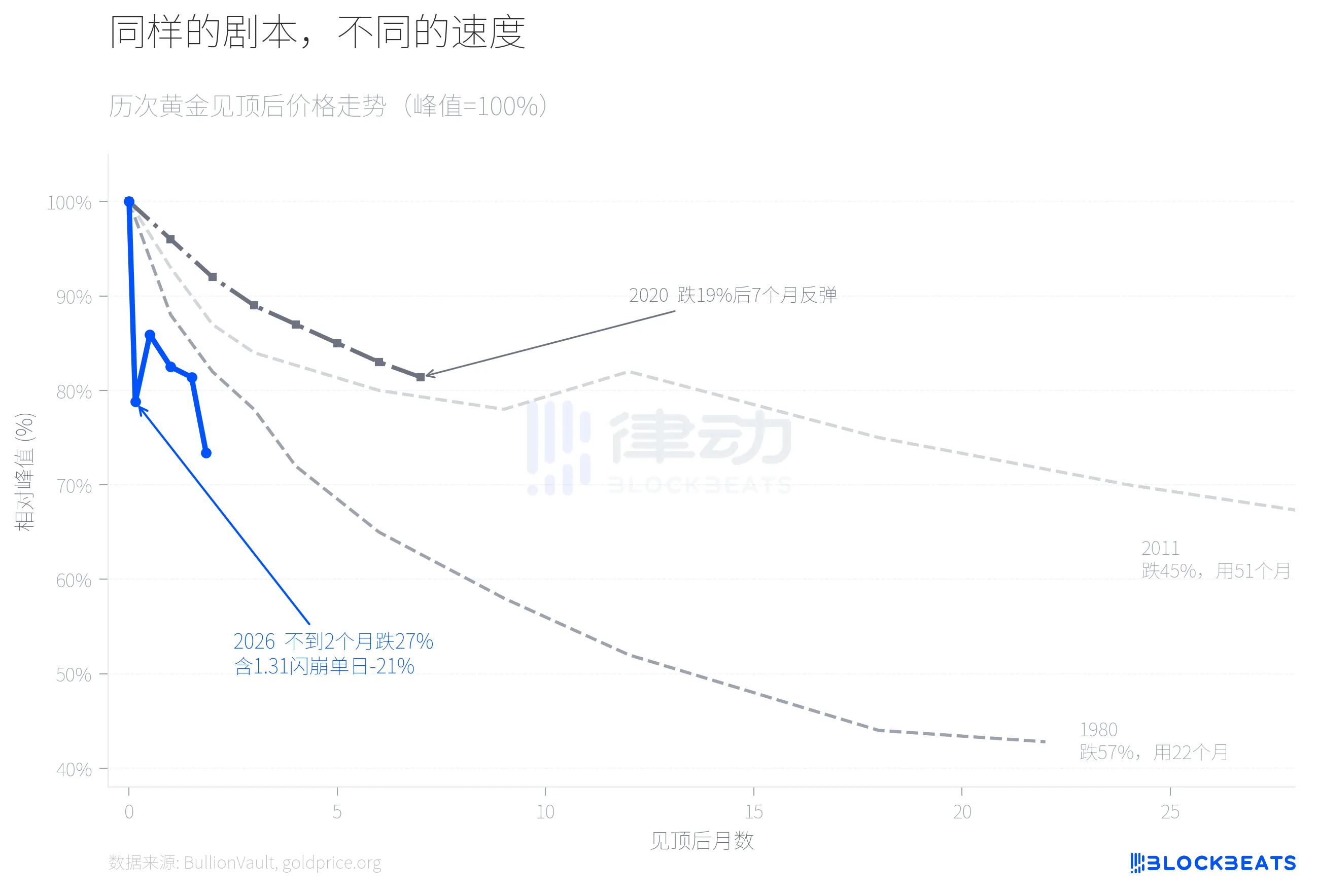

According to historical data compiled by the precious metals analysis firm Auronum, in 1980, Volcker pushed the federal funds rate to 20%, gold dropped from a peak of $711 to $304, a 57.2% decline, taking 456 trading days. In 2011, amid expectations of QE exit and a strengthening dollar, gold fell from $1,999 to $1,049, a 44.6% decline, taking over 4 years. The pullback in 2020 was milder, with vaccine rollout and a rebound in US bond yields causing gold to fall 18.6% from a peak of $2,067, but resuming its upward trend 7 months later.

The pullback in 2026 is currently around a 27% decline, exceeding that of 2020 and approaching that of 2011. However, in terms of speed, it is the fastest of the four.

Overlaying the price trends of the four pullbacks, the differences are clear. In 1980, it took nearly two years to complete the major decline, and in 2011, it took over four years. In 2026, the gold price completed a 21% retracement on the 5th trading day after peaking, followed by a brief rebound, but accelerated its decline to around $4,100 in the third week of March, expanding the cumulative decline to 27%. The flash crash on January 31 was a turning point. According to data from the world's largest precious metals trading platform BullionVault, gold fell more than 10% that day, silver plummeted 13.7%, and the iShares Silver ETF (SLV) saw trading volume exceed $40 billion, ranking it as one of the largest single-day trading volumes in US securities history. Former ICBC Tokyo Precious Metals Business Director Bruce Ikemizu commented that, having observed this market for 40 years, he has "never seen this level of volatility before."

Why Was This Speed So Abnormal? One key variable was CME's shift on January 13 to a contract value percentage margin system from a fixed amount for COMEX. According to CME Group data, gold futures margins were raised from 8% to 9%, and silver from 15% to 18%. In a rapidly rising market, a percentage margin system means that as prices increase, the required margin also increases, creating a self-reinforcing deleveraging mechanism. As reported by goldsilver.com, over 67 million ounces of silver paper contracts were forcibly liquidated within minutes on the day of the flash crash.

Silver's performance was one dimension that was overlooked in this round of plummeting.

In April 2025, the gold-silver ratio briefly exceeded 100:1, with silver significantly lagging behind gold. Silver then saw a surge, achieving a full-year gain of 147% (compared to gold's 67%) after hitting a peak of 121.67 USD per ounce, bringing the ratio down to around 46:1, the lowest level since 2013.

Then everything reversed on January 31. According to data from that platform, silver experienced a one-day drop of 13.7%, with a cumulative decline reaching 41.1% from the peak of 121.67 USD, far exceeding gold's 26.6% during the same period. This was a rare precious metal one-day swing not seen since the 1980 Hunt Brothers incident ("Silver Thursday"). As of March 23, silver was trading around 67.4 USD, and the gold-silver ratio had rebounded from its low of 46:1 to around 61:1. The rally in silver that took 9 months to materialize was mostly wiped out in less than 2 months.

The core reason for this asymmetry lies in silver's dual nature. On one hand, according to a CME Group research report, solar panel capacity grew by 18% YoY, indicating silver's industrial demand is still structurally expanding. On the other hand, the leverage ratio in the silver market is much higher than in gold, and CME's margin increase from 15% to 18% directly triggered large-scale liquidation. The industrial fundamentals remained unchanged, but the financial leverage broke first.

The last signal worth noting is the divergence in fund structure.

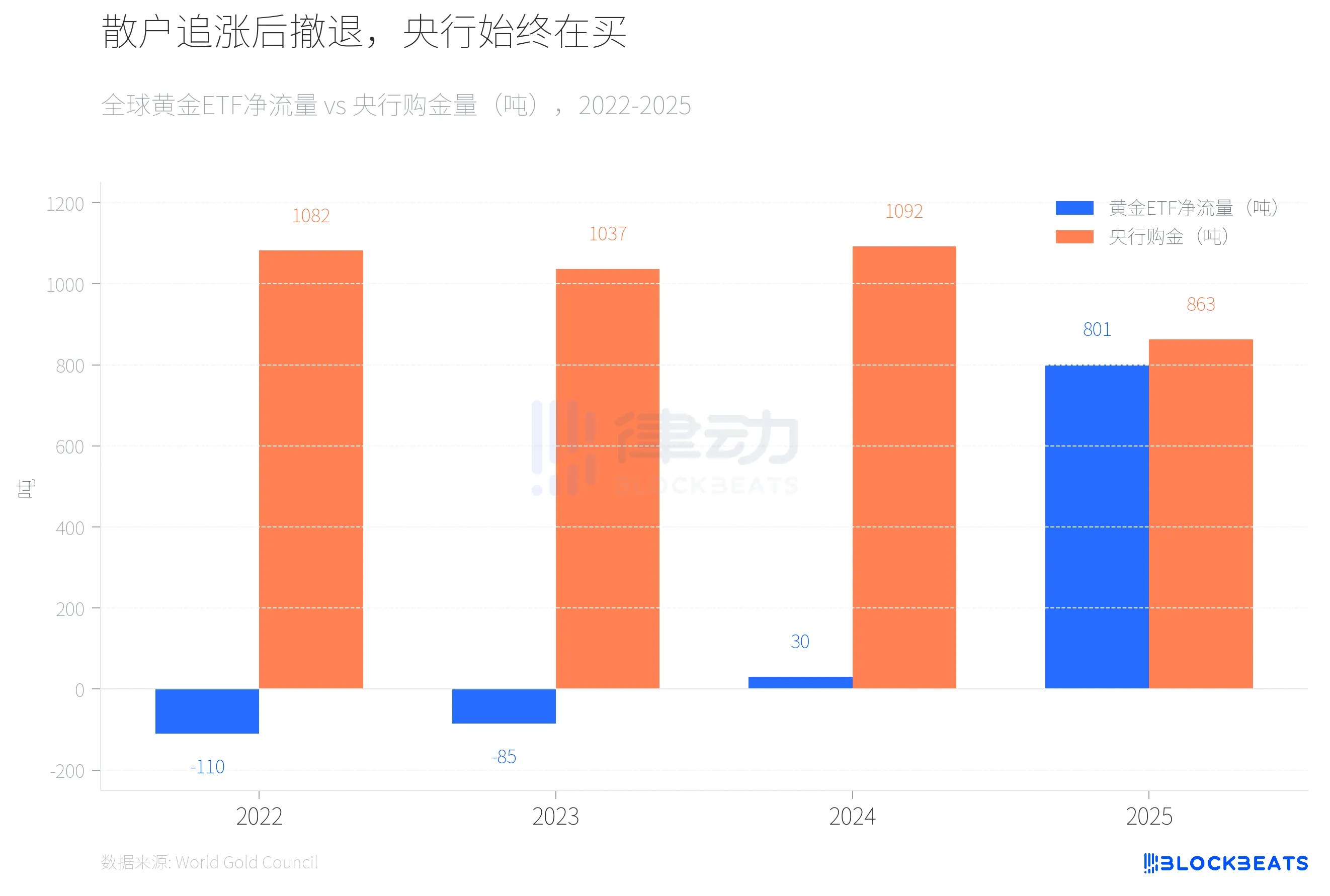

From 2022 to 2023, global gold ETFs saw two consecutive years of net outflows (-110 tons and -85 tons, respectively), while central bank gold purchases exceeded 1,000 tons for two consecutive years. In 2024, ETF funds turned positive but on a small scale (30 tons), while central banks continued their high-level purchases at 1,092 tons. The situation dramatically changed in 2025; based on World Gold Council data, global gold ETFs saw a record net inflow of 801 tons for the full year, doubling their assets under management to $559 billion.

Then the retail money started running. According to the Canadian business media Chronicle Journal, the SPDR Gold Trust (GLD) saw a single-day net outflow of $2.91 billion on March 4, marking the largest single-day outflow since 2016, with 25 tons of gold lost in 7 days. Meanwhile, according to the institution's annual report, global central banks bought 863 tons of gold by 2025, a 21% decrease from 2024 but still well above the 2010-2021 average level (473 tons). The same report shows that the Polish central bank, with a purchase volume of 102 tons, became the world's largest buyer for the second consecutive year, followed closely by Kazakhstan (57 tons) and Brazil (43 tons).

According to a March research report by J.P. Morgan, the bank maintains its year-end 2026 gold price target of $6,300. However, according to the IEA's March Oil Market Report, the blockade of the Strait of Hormuz has led to a global oil supply reduction of about 8 million barrels per day, equivalent to nearly 8% of global demand. The IEA called it the "largest supply shock in the history of the global oil market," with member countries initiating the largest-ever 400 million-barrel release from strategic reserves.

For central banks of oil-importing countries, the priority of dealing with oil price shocks may be higher than continuing to increase their gold holdings. In the previous three peaks, global central banks were not net buyers of gold. They bought 863 tons in 2025, but no one knows the number for 2026 yet.

You may also like

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.