Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Rising over 40% against the trend, how to understand the logic behind USUAL’s rise?

Original author: @hmalviya9, founder of dyorcryptoapp

Original translation: Ismay, BlockBeats

Editor's note: More and more competitors have emerged in the stablecoin track. From the beginning of December to now, from listing on Binance to the official announcement of cooperation with BlackRock, Usual has performed well in the market with its innovative economic model and high return potential. Today, USUAL broke through $1.2, setting a new record high. This article deeply analyzes the token economics, profit mechanism and potential risks of $USUAL, aiming to provide readers with a comprehensive understanding to help everyone make informed decisions in the rapidly developing crypto market. Whether considering investment or observing market trends, understanding its core mechanism is key.

The following is the original content:

$USUAL is one of the most important launches of this cycle, and the initial performance is very promising, so should you buy it or ignore it?

I started paying attention to USUAL a few months ago when I was researching new stablecoins. What makes USUAL unique is its clear story: Tether on chain, distributing income to token holders. Tether has made more than $7.7 billion in profits so far this year, which is almost more than BlackRock.

If USUAL can achieve this goal, even just 10% of it will mean $770 million in profits. And the best part is that 90% of the revenue will be distributed to token holders and stakers in the form of $USUAL.

Returns are paid in $USUAL, so every time someone stakes USDO (their stablecoin), $USUAL tokens are constantly issued.

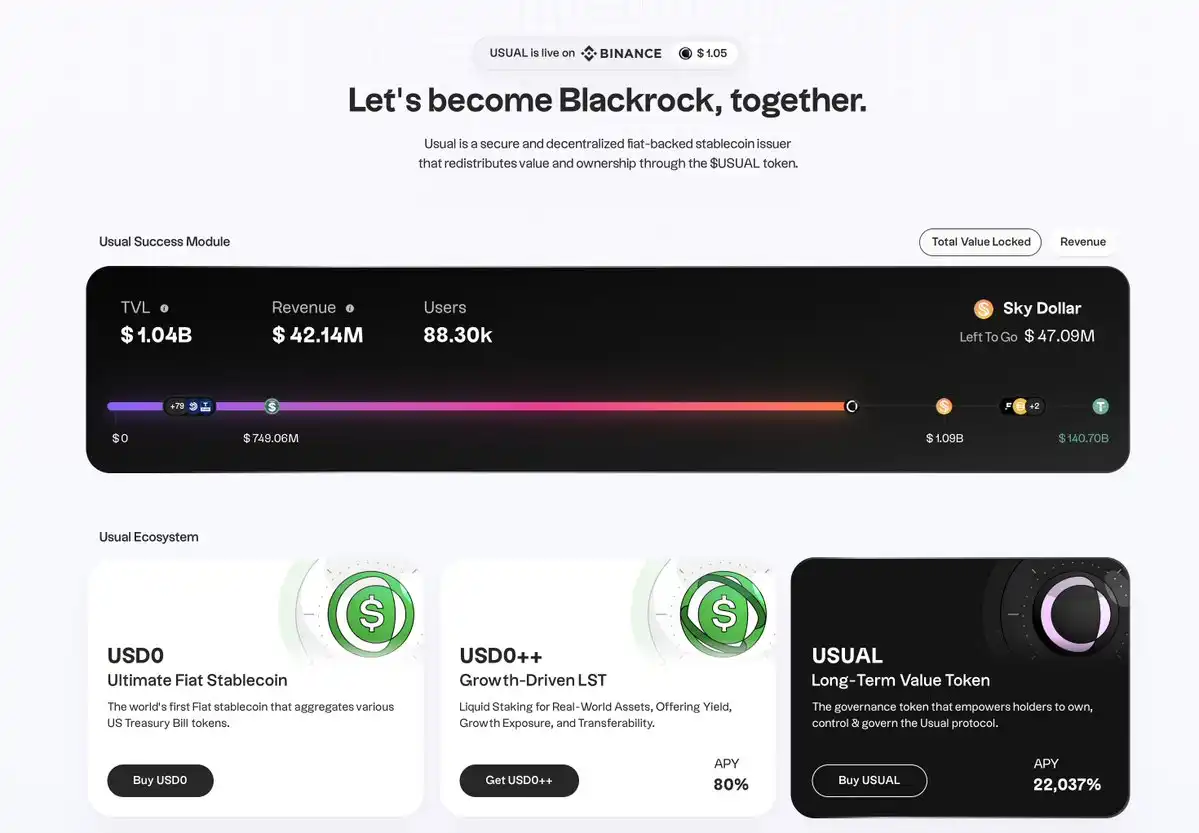

USDO is a stablecoin backed by US Treasuries that generates returns through Treasuries, and these returns are distributed in the form of $USUAL and USDO.

USUAL Money mentioned that when $USUAL's cash flow reaches a certain target, they plan to control the issuance of $USUAL and ensure that the continuous issuance rate is lower than the revenue growth rate. Initially, the issuance will be high, but over time, the issuance will gradually decrease.

USUAL offers two other tokens in addition to the governance and staking token $USUAL.

USDO++: This is the liquidity token you get after staking USDO. USDO holders need to stake USDO for 4 years to mint USDO++. USDO++ holders will receive 45% of the $USUAL issuance.

USUAL issues new $USUAL tokens whenever new USDO++ is minted. This is a core part of their flywheel mechanism. The TVL (Total Value Locked) of the protocol also tracks the value of USDO++ minted in the protocol.

The higher the TVL, the more revenue the protocol generates, which will eventually be paid to USDO++ holders in the form of $USUAL tokens.

The issuance rate of $USUAL will decrease as more users adopt it, reducing the number of tokens issued per dollar locked.

This reduction will increase the yield per token, which will naturally drive the price of $USUAL up.

The higher annualized yield (APY) on USDO++ will attract more people to stake USDO. The current APY is around 80%, so we may see TVL rise in the coming days. The current TVL is around $900 million, and 87.47% of USDO has been staked as USDO++.

USUAL also has a staking token called USUALx, which provides three forms of yield: USDO rewards from revenue, 10% of $USUAL issuance, and 50% fee share from unlocking modules.

When USDO++ holders decide to unlock before expiration, the protocol will also initiate the destruction mechanism of $USUAL.

They need to destroy a portion of the $USUAL supply to unlock.

As mentioned in the USUAL Money whitepaper, we do face two serious product risks:

The market price of $USUAL (the main reward token) directly affects the benefits in the ecosystem, including rewards and liquidity incentives related to USDO++. If the price drops significantly, it may damage the competitiveness and user attractiveness of the ecosystem. Due to its inflationary nature, there is also a risk of hyperinflation.

To this end, the DAO can mitigate this risk by adjusting the minting rate to regulate the issuance, ensuring economic stability and sustainability.

USDO++: These locked tokens lack a costless arbitrage mechanism to maintain their anchor, which can lead to price volatility. However, this risk has been minimized through strong liquidity in the secondary market, as well as liquidity provision incentives and early redemption mechanisms. In addition, the price floor redemption mechanism limits extreme volatility, ensuring stability and market efficiency.

Overall, as long as the price of $USUAL is attractive, the protocol can attract more demand for USDO and USDO++. The greater the demand for its stablecoins, the more revenue it will ultimately generate, which will be distributed to USDO++ holders, USUALx holders, and other participants.

Currently, USUALx has an annual interest rate of about 28,000%, which may attract initial demand and create early market heat.

However, in the long run, the key lies in how the USDO anchoring mechanism is stabilized and how long $USUAL can continue to attract demand.

In terms of token economics: approximately 90% of the tokens are allocated to the community, of which approximately 64% are used for inflation rewards, which will adjust the issuance plan based on dynamic demand. Currently, approximately 12.4% of the tokens have entered circulation.

You may also like

From x402 to MPP: Cloudflare's crucial vote, will it go to Coinbase or Stripe?

BlackRock CEO issues annual open letter: The wave of tokenization has arrived, and we will lead this trend

When Backpack backstabs the community

When gold is no longer a safe haven, and Bitcoin continues to panic

Trump, the World's Largest Oil Trader

If the US and Iran have not reached an agreement in 5 days, what other cards does Trump have?

Tether Whale Dumps £12 Million, Backing Crypto’s ‘British Trump’

Ethereum Foundation Post: Rethinking the Division of Work Between L1 and L2 to Build the Ultimate Ethereum Ecosystem

Two Major Prediction Market Platforms Unite Rarely, What Is the Story Behind This New Fund?

Dragonfly Partners: Most agents will not engage in autonomous trading, how can crypto payments prevail?

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a btc-42">bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.

The US AI Startup Is Loving China's Open Source Model