Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

a16z Visual: AI Cost Halving, Usage Doubling, U.S. 30-Somethings Enter the 'Adulthood Delay' Era

Original Title: Charts of the Week: DExit . . . real or feigned?

Original Source: a16z New Media

Original Translation: DeepTech TechFlow

DeepTech Summary: This week's a16z Chart Report covers four topics, each worthy of its own article: AI cost declines triggering the Jevons effect, the true scale of Big Tech capital expenditure, Kalshi prediction markets outperforming expert forecasters, and the comprehensive delay of American 30-something milestones. With solid data sources and a calm, restrained perspective, it is a high-quality reference for understanding the current intersection of technology and macro trends.

DExit... A Real Trend or an Illusion?

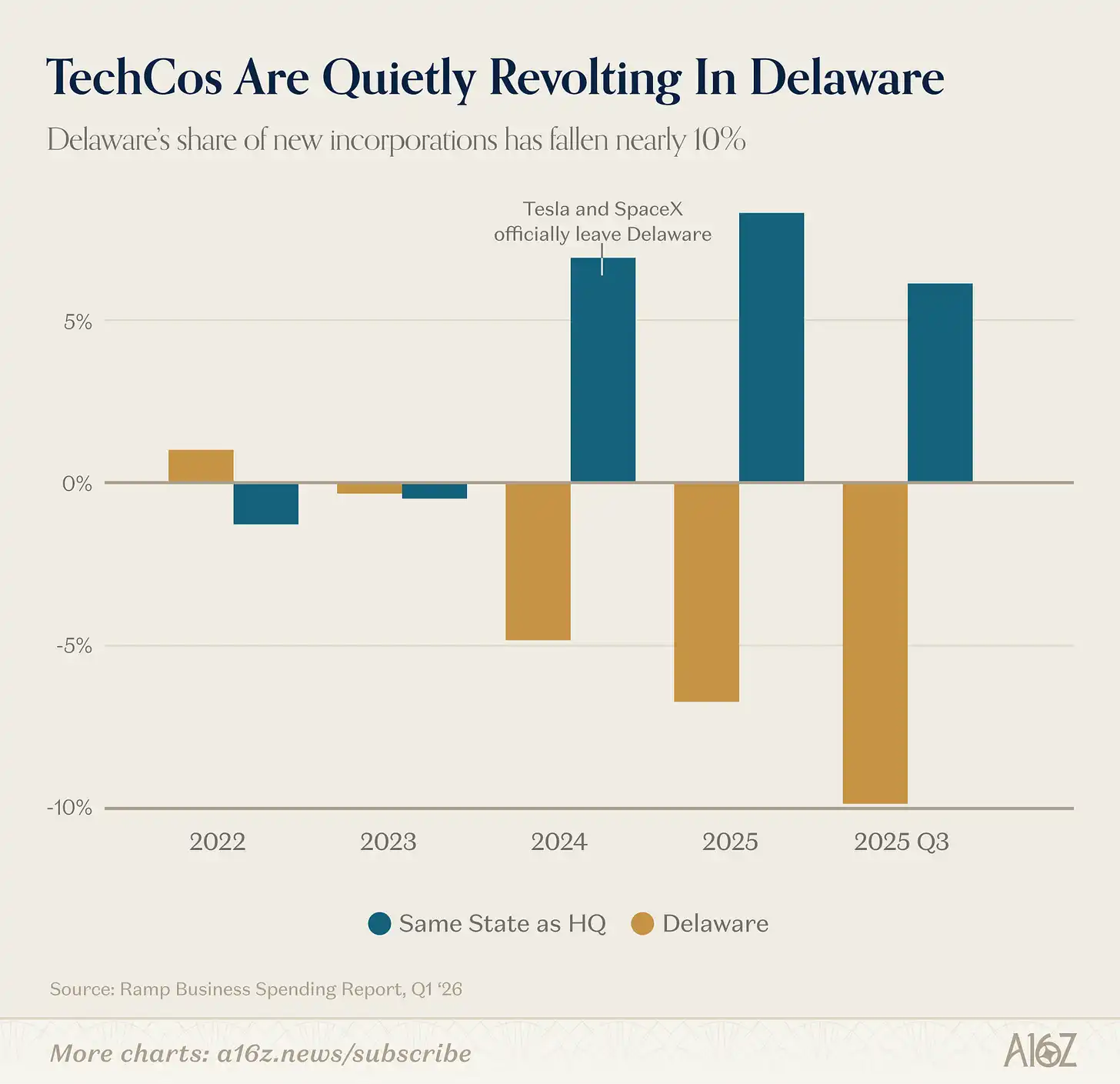

Delaware remains the top choice for U.S. company incorporation, but this position is quietly slipping:

According to Ramp's data, Delaware's share in new company registrations has been declining since 2023, with a roughly 10% drop in the third quarter of 2025.

History does not merely repeat itself, but it often rhymes... maybe.

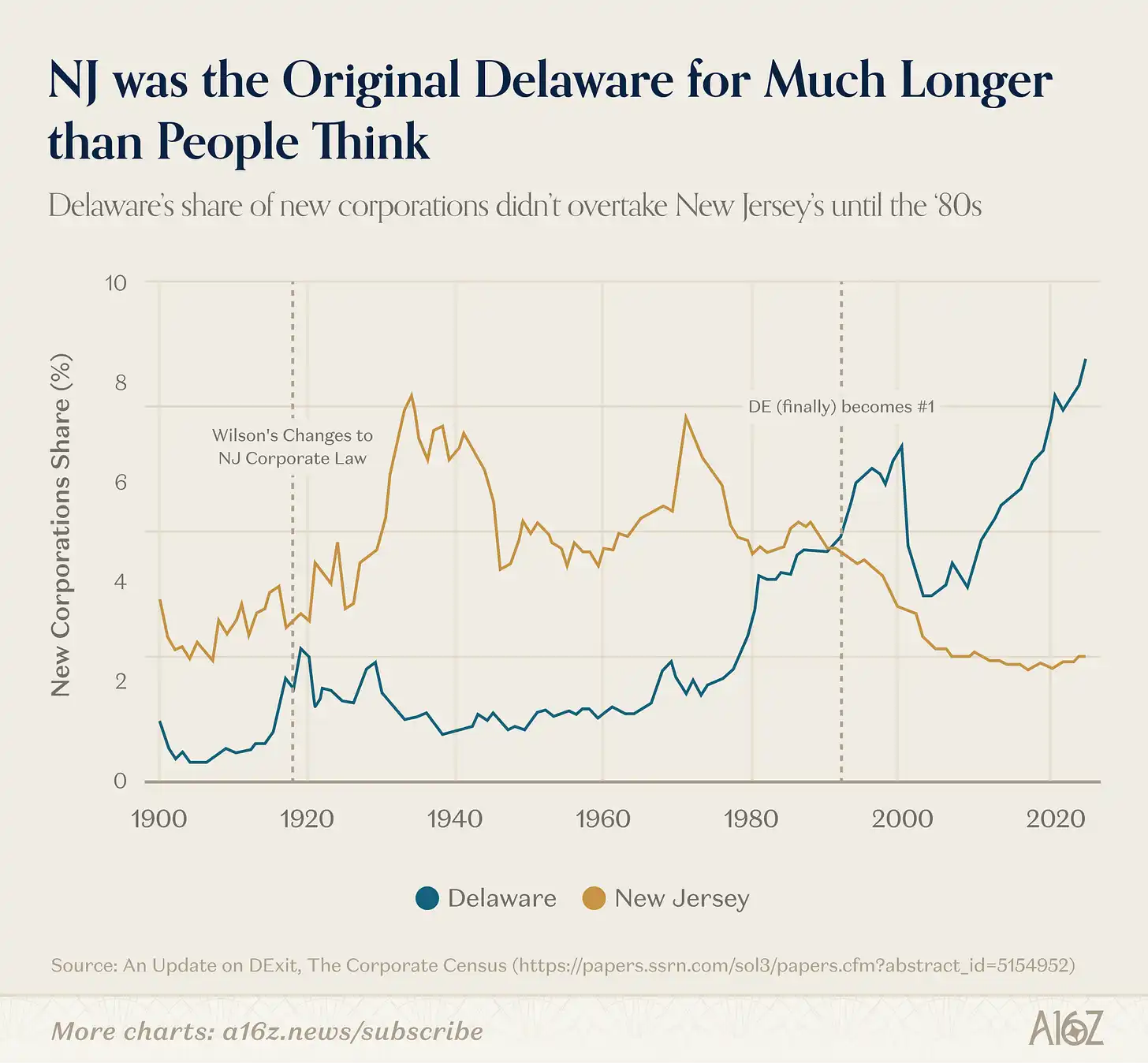

Delaware has not always been the mecca of corporate registration.

About a century ago, Delaware replaced New Jersey—the original "mother of trusts"—as the preferred destination for company registration. New Jersey lost its edge because then-Governor Woodrow Wilson sought to curb "corporate abuses," significantly deteriorating New Jersey's business environment. Delaware's corporate law was modeled after the pre-Wilson era New Jersey laws and was naturally welcoming to fleeing enterprises. Subsequently, by joining the Delaware Chancery Court, it spent nearly 100 years building a reputation as a mature and impartial venue for resolving corporate and investor disputes.

However, something that took a century to build started to shake in just a few years. Regardless of right or wrong, the Delaware Chancery Court has taken a more lenient stance on shareholder litigation in recent years (especially in several high-profile cases, including but not limited to Tesla), prompting companies to genuinely move their registrations elsewhere. Good night, and good luck, Delaware.

This is at least the mainstream narrative, but other data paints a more complex picture.

First, even the foundational myth of Delaware is not entirely accurate.

It wasn't until the 1980s (about 60 years into Governor du Pont's reign) that Delaware truly pulled ahead of New Jersey to become the top state for business entities in the U.S.:

New Jersey's dominance lasted far longer than the mainstream narrative describes. Delaware's eventual leap forward was likely catalyzed by passing a series of laws related to directorial responsibility that made it especially attractive to public companies, along with network effects that continually reinforced themselves, generating its own momentum.

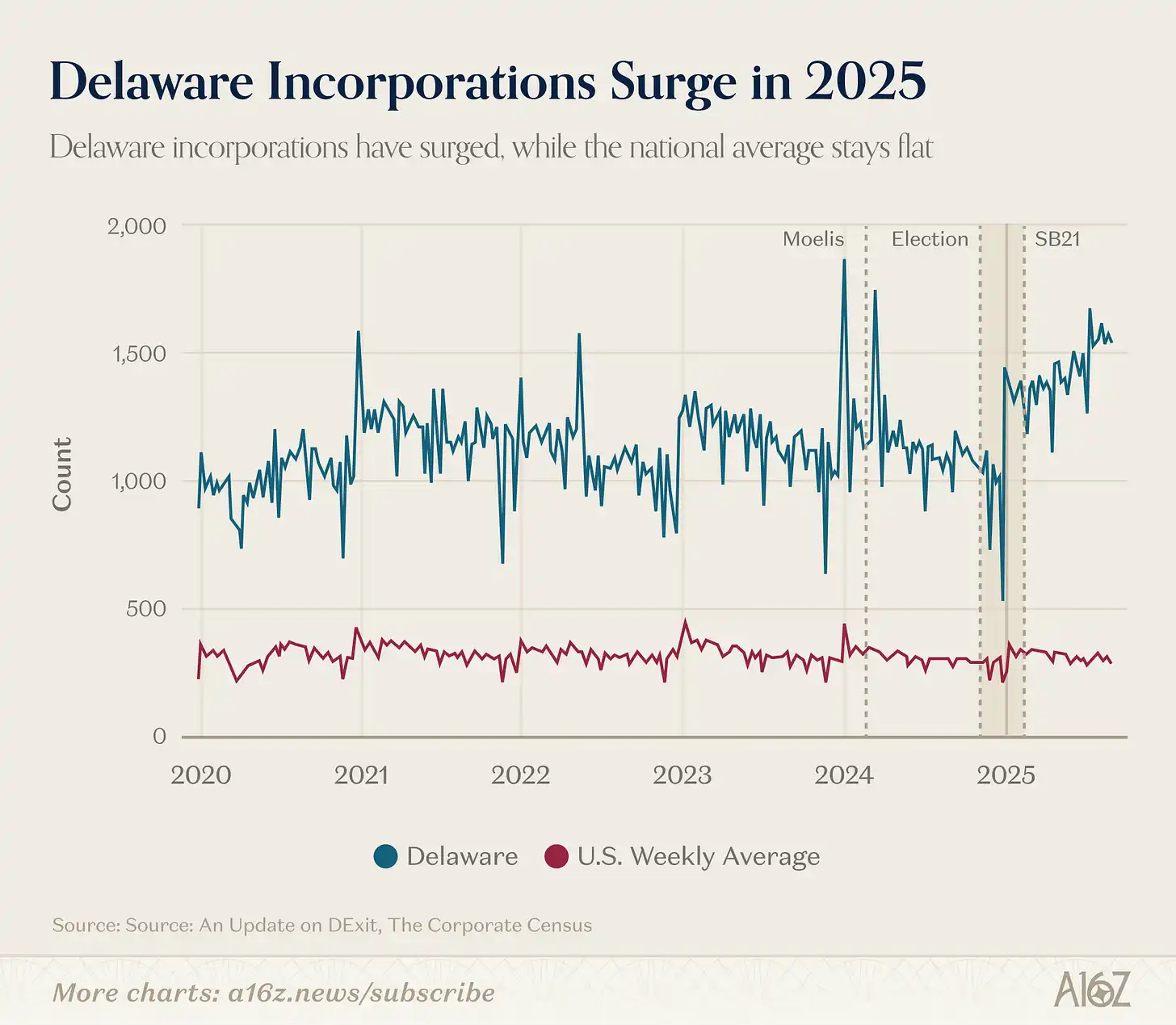

Second, regardless of what's happening with high-profile public companies (and companies in the Ramp data), Delaware as a whole still seems to be doing well, and more than that:

According to data released by the Harvard Law School Forum on Corporate Governance, from the end of 2024 to 2025, Delaware's share of total U.S. businesses actually saw a significant increase.

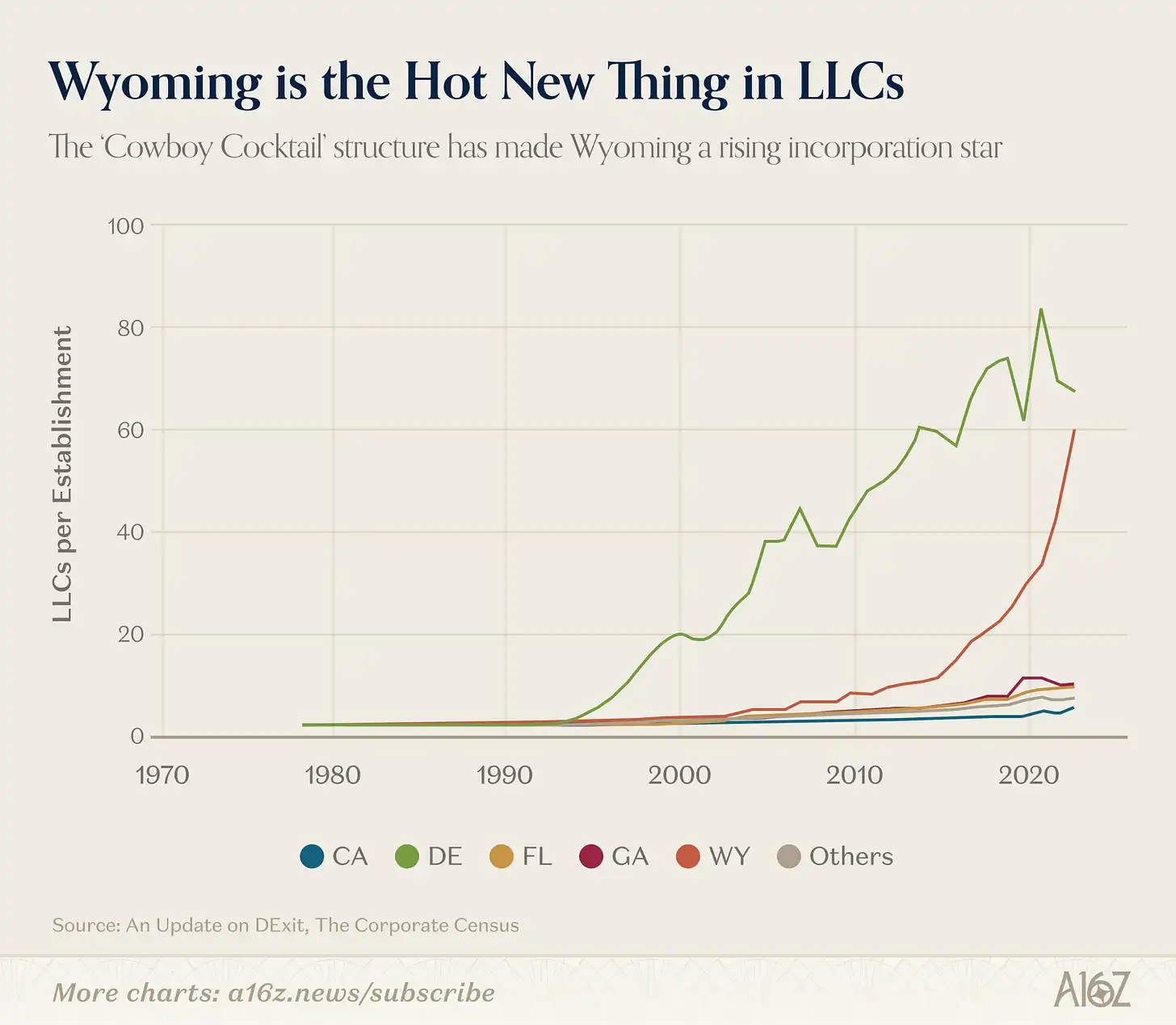

In fact, if you're looking for a clear "DExit" case, it's probably this, and it has nothing to do with Tesla but instead involves a specific corporate form:

LLCs in Wyoming started to skyrocket around 2015.

Why? This likely has to do with specific asset protection and privacy provisions in Wyoming's LLC laws, which the state itself markets as a "Cowboy Cocktail" of company structures.

The key takeaway here is not to say that DExit isn't happening (because at least some data suggests that it is happening — even if only a few high-profile companies leaving carries weight), but the reality is certainly more complex than what the mainstream narrative presents.

The reality is that Delaware still enjoys the advantage of being the default option, not to mention all the network effects tied to it that are hard to disrupt.

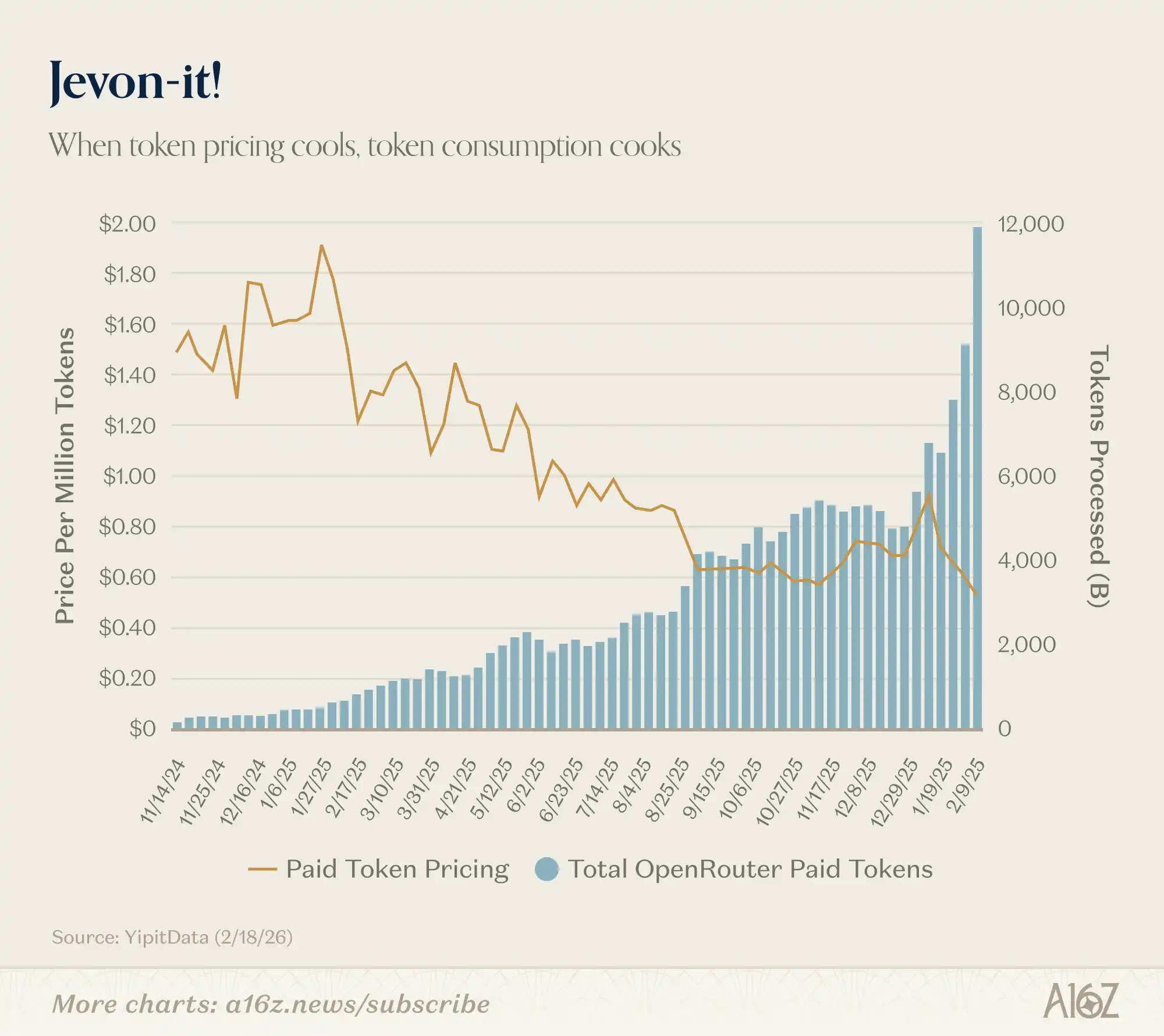

We've posted earlier versions of this chart, but with more data, the effect is even more striking.

Token Costs Down, Token Consumption Up:

Since the beginning of this year, the price of paid tokens has dropped from about $0.90 per million tokens to $0.50, while the number of tokens processed has almost doubled, increasing from about 6,000 to 12,000.

This is a typical Jevons Paradox. The cheaper AI gets, the more AI we use. Delightful.

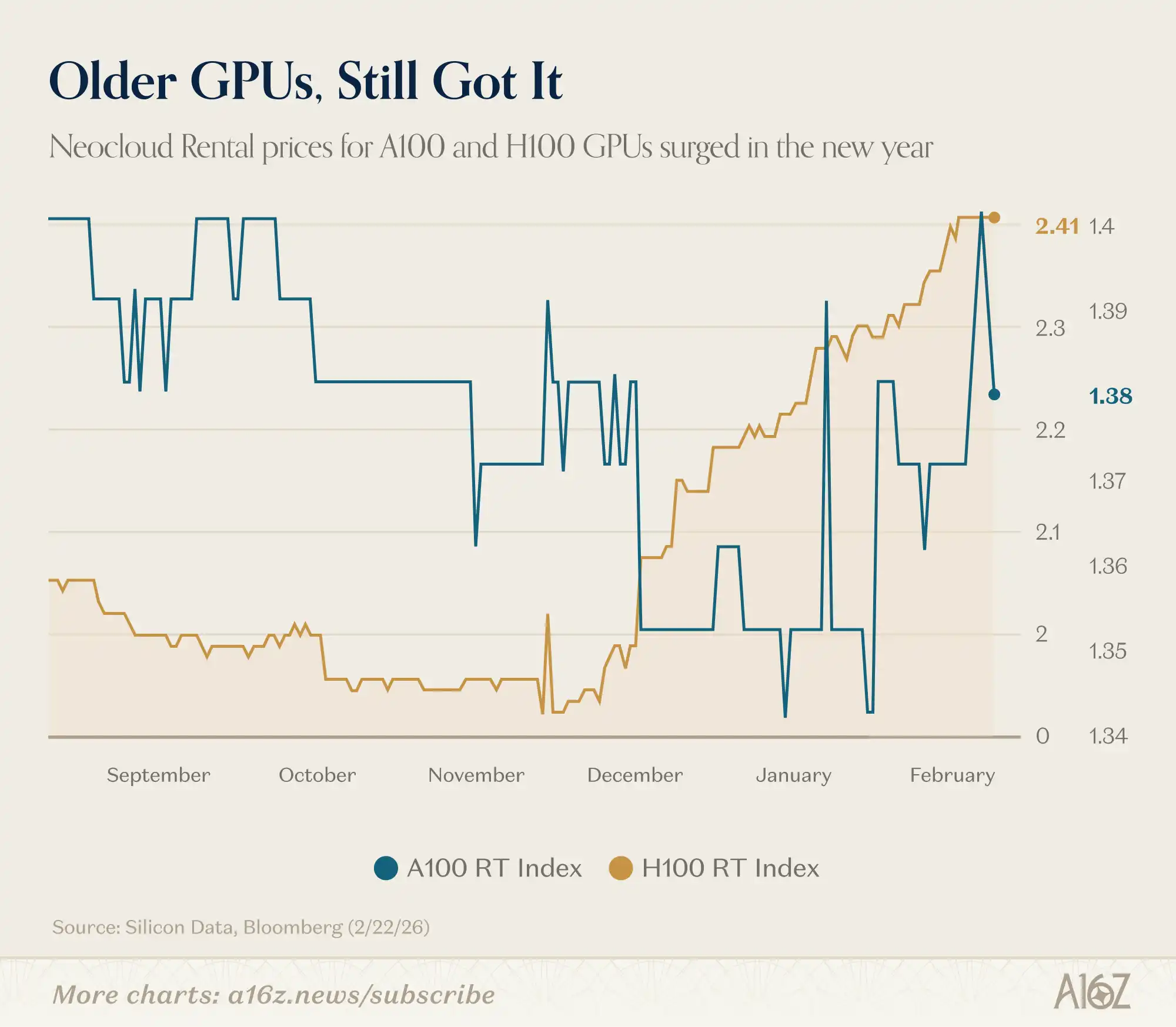

Remember when someone said that once newer and better GPUs are released, no one would want the old ones anymore?

Well, it seems that's not quite the case:

According to Silicon Data, the rental prices of NVIDIA H100 and A100 have both increased this year.

There are no signs in the market of an oversupply of mining power. It seems like the surface of the existing demand has not even been scratched yet.

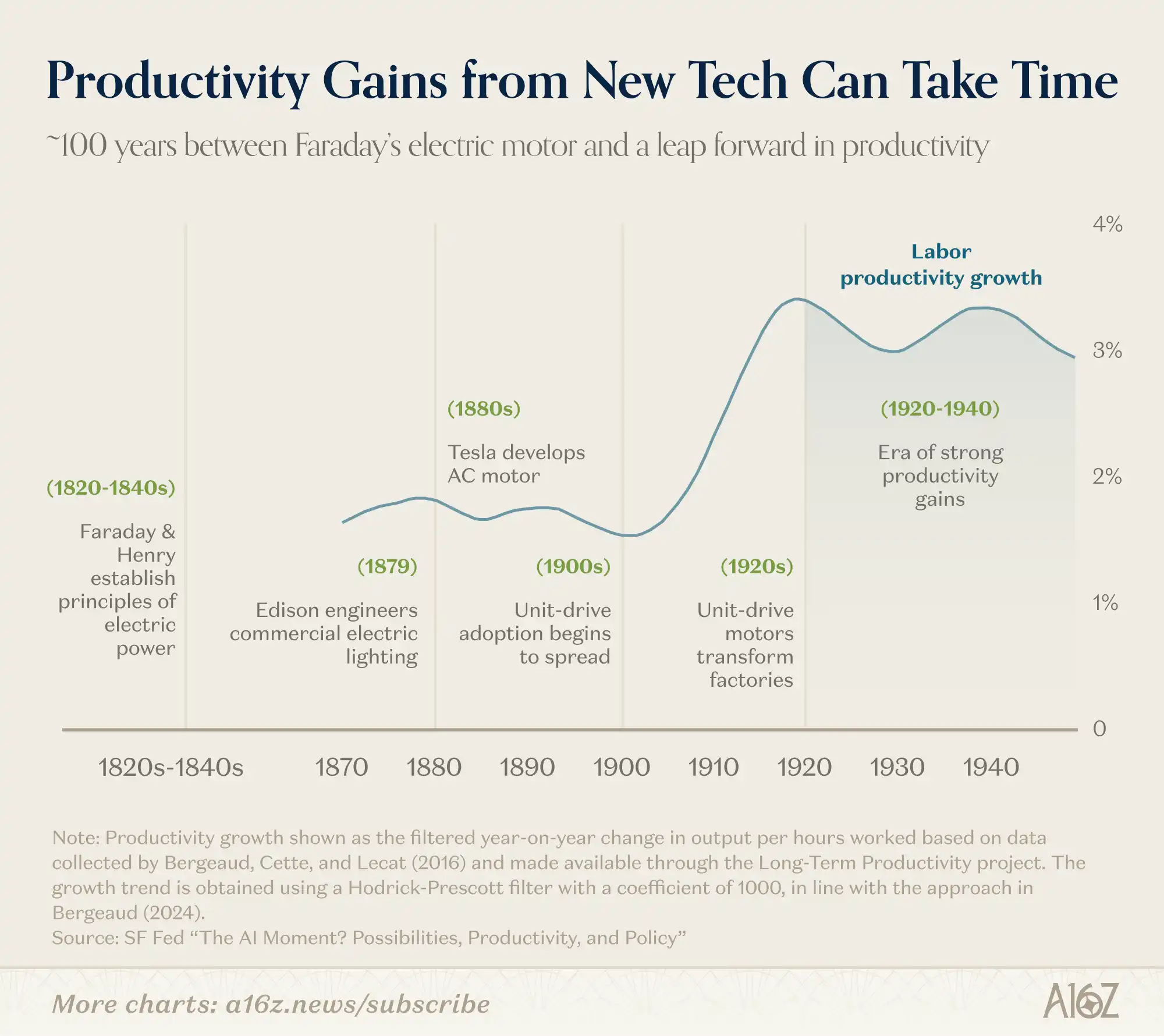

While this comparison is not perfect, if history is any guide, it may take some time to truly "see" what the AI-driven "economy" will look like:

From Faraday and Henry's initial discussions of electricity to the real surge in industrial productivity in the first half of the 20th century, it took about 100 years.

Since the 1820s, the pace of technological iteration has indeed accelerated, but the variables involved in a platform-level shift are still extremely numerous.

Roy Amara had a famous saying: "We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten years."

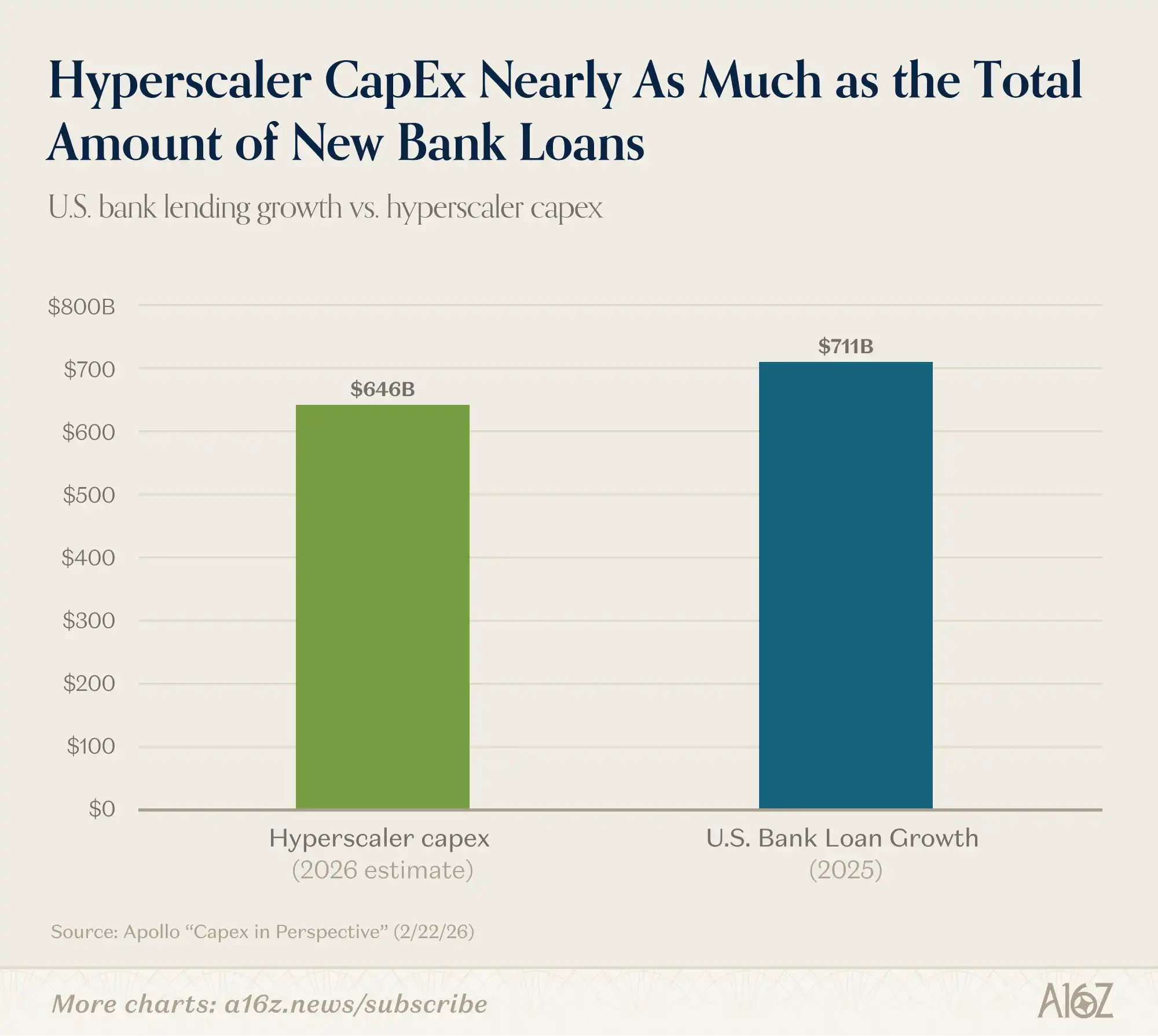

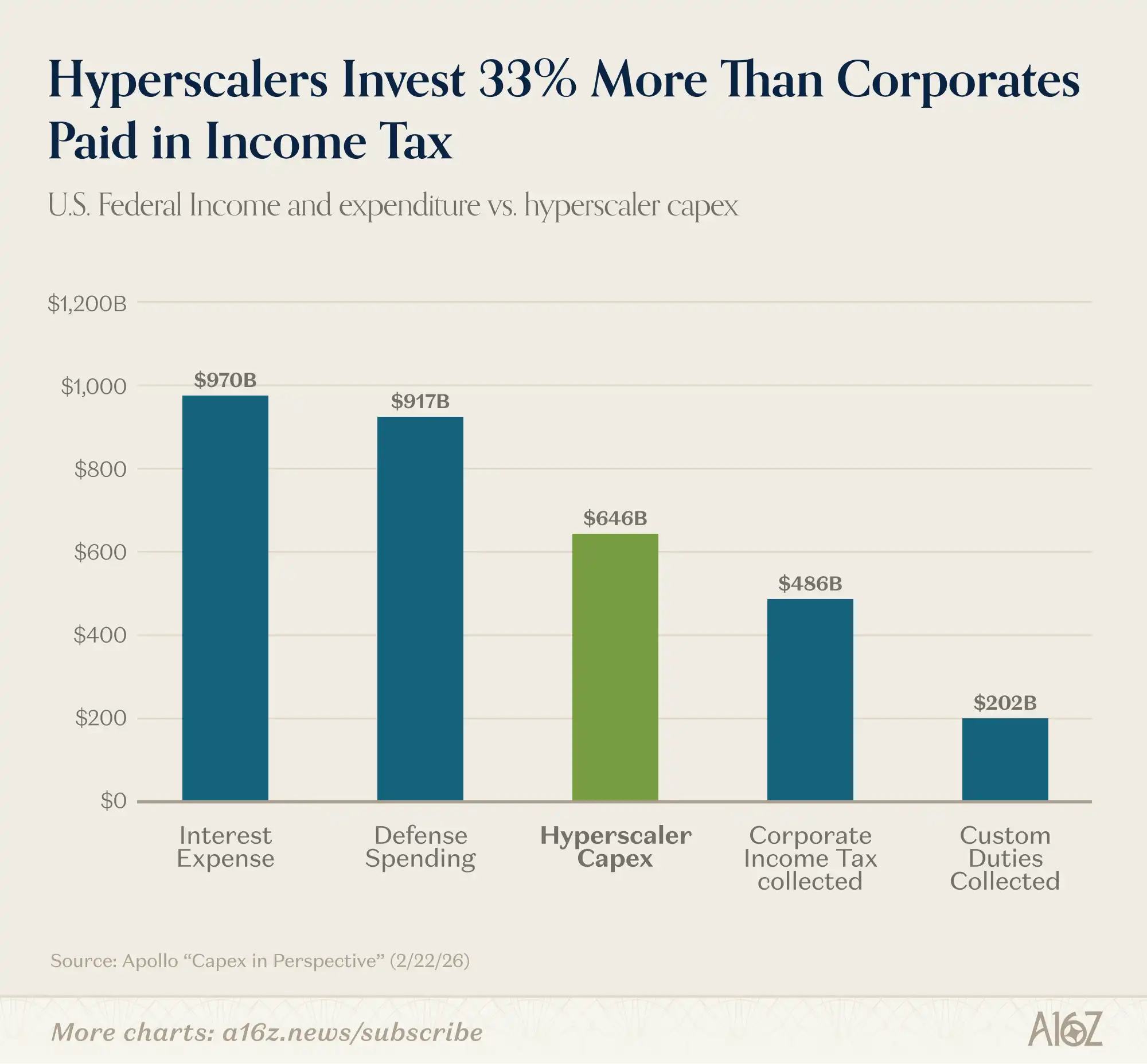

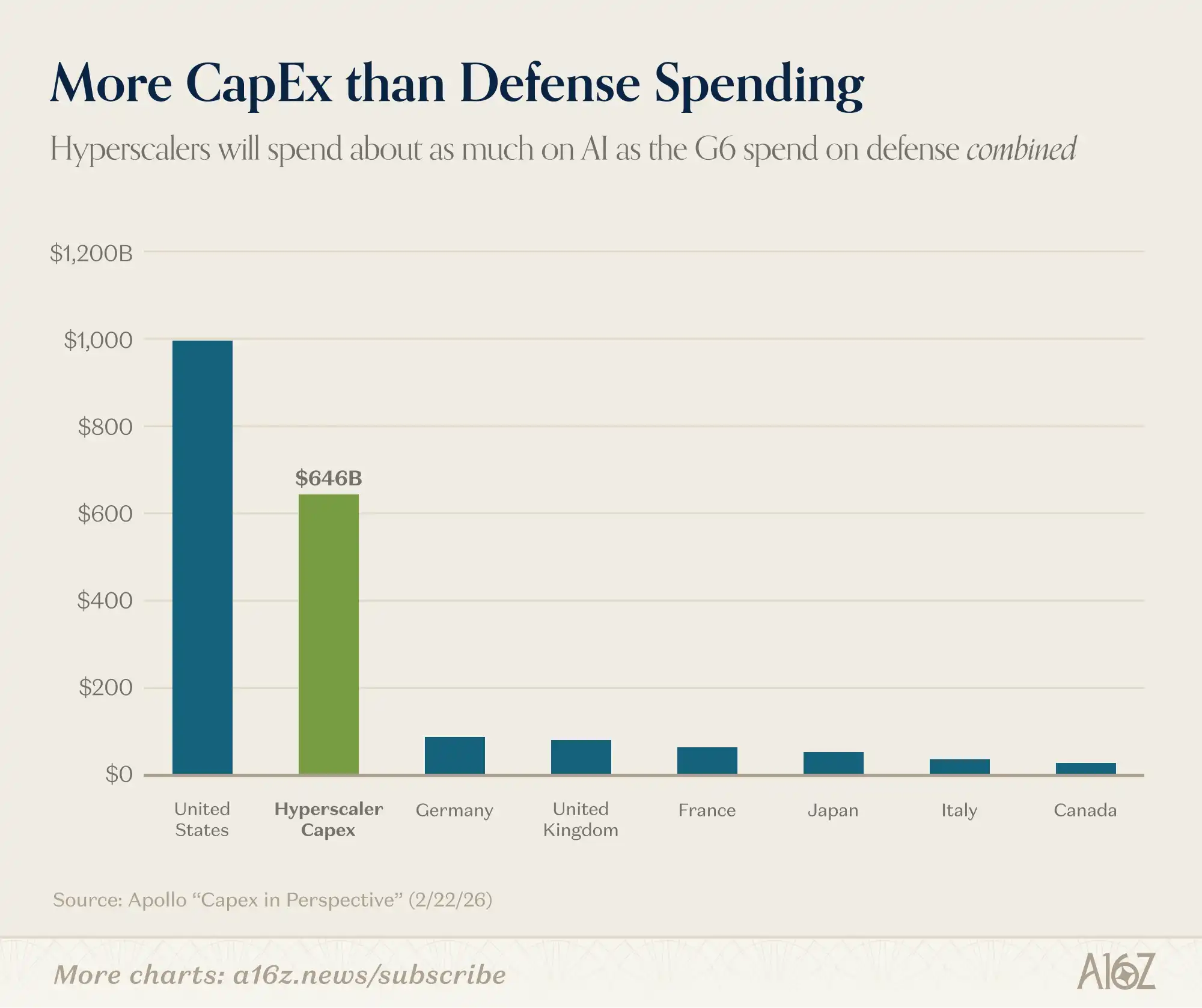

Capital Expenditure, Plotted on a Graph

Look at this set of timeless data: AI capital expenditure is substantial.

Consider the following comparisons:

AI capital expenditure in 2026 is projected to be nearly equivalent to the total net new loans of all U.S. banks in 2025:

Capital expenditure is around 33% higher than the total corporate income tax revenue in the U.S. and about three times the total tariff amount:

Capital expenditure is about six times the total military budget of any non-U.S. G7 member:

So, yes, the scale of capital expenditure is indeed substantial.

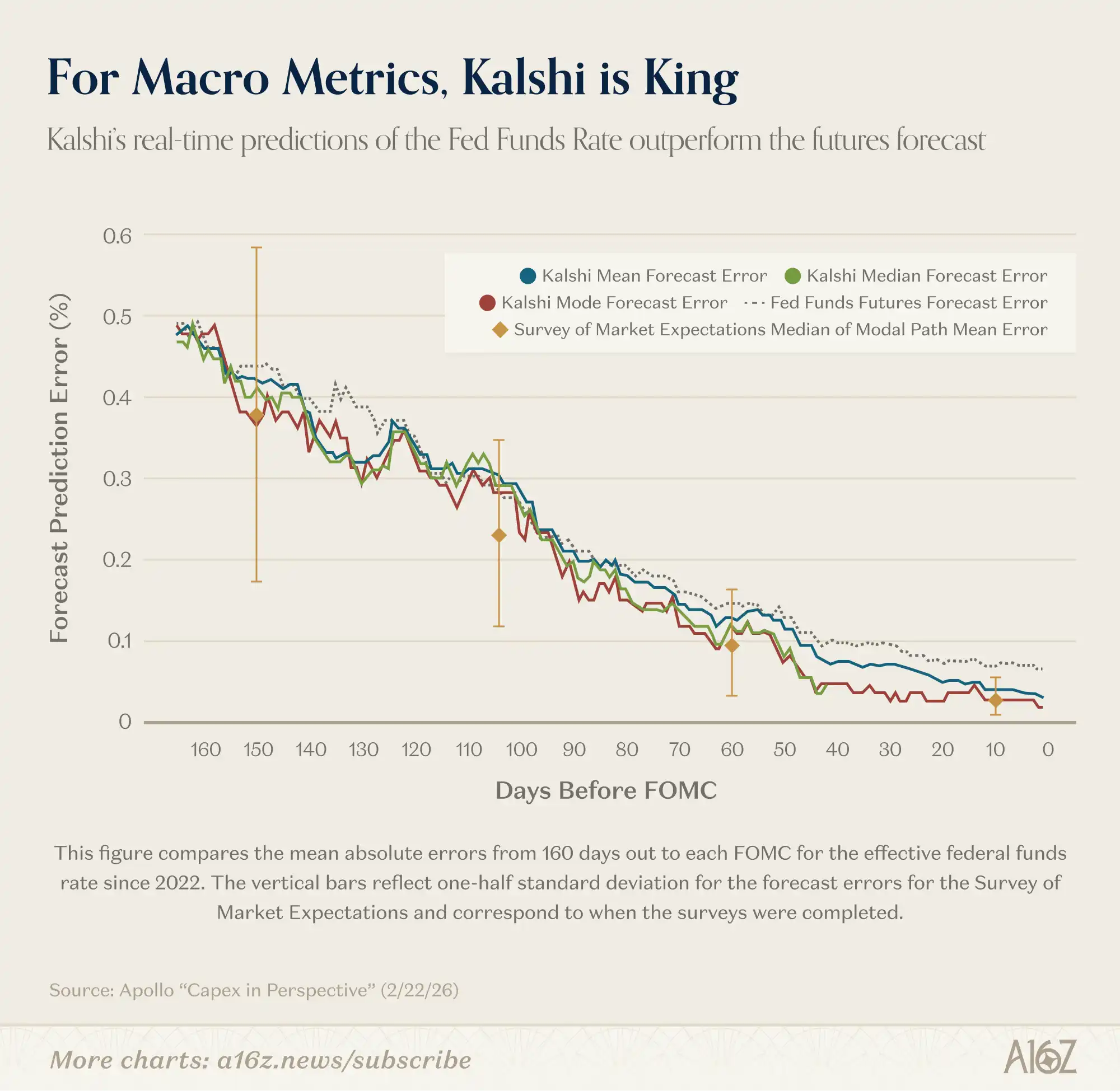

Kalshi Makes Inroads in Macro Forecasting

A Fed researcher believes prediction markets are quite good.

At least on one measure, Kalshi's performance in forecasting the federal funds rate has surpassed that of professional forecasters:

For the 150-day-ahead (i.e., post 3 FOMC meetings) federal funds rate forecast, Kalshi's mean absolute error is very close to that of professional forecasters. But unlike surveys that provide a modal path snapshot only every six weeks, Kalshi provides continuously updated full probability distributions... We find that Kalshi's median and mode forecasts are perfectly accurate at the forecast time of day prior to the FOMC meeting, a statistically significant improvement over federal funds futures forecasts.

In other words, while all forecasters start about the same, Kalshi's continuously updated forecasts optimize over time, ultimately achieving a perfect forecast record the day before the rate is announced. Additionally, Kalshi's performance surpasses that of the futures market forecasts.

Kalshi's advantage extends beyond the federal funds rate. As Fed researchers point out, since macroeconomic indicators like inflation, growth, and unemployment lack other options markets, Kalshi is the only place to provide a "high-frequency, continuously updated, richly distributed 'benchmark' where 'the crowd' opines on where these economic indicators are headed."

That sounds pretty important.

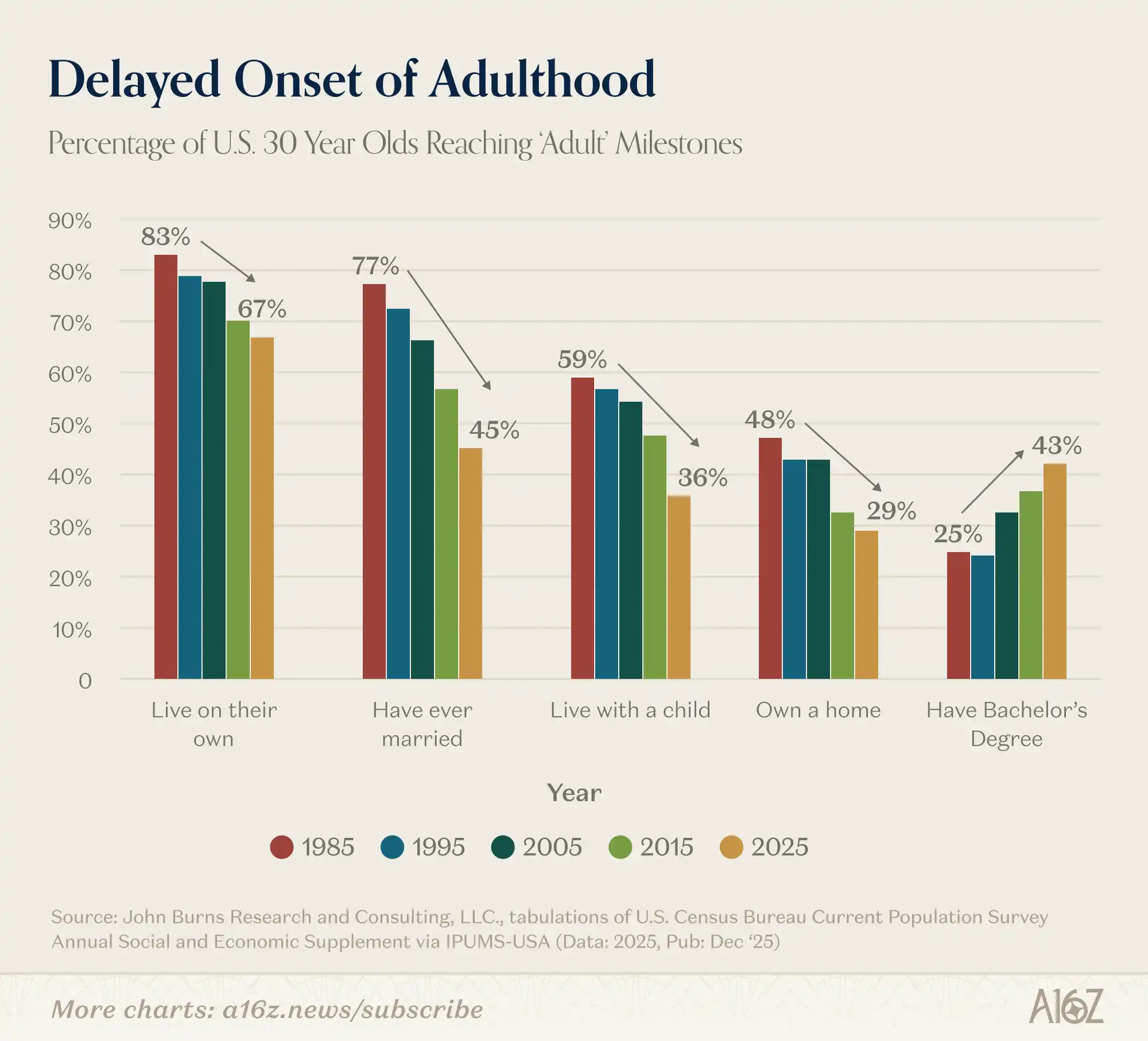

The Age of Delayed Adulthood

Here is a thought-provoking chart with a (small) commentary:

The share of the 30-year-olds achieving major life milestones has been on a steep decline, at least since the 1980s.

Among 30-year-olds, fewer and fewer are:

Living independently;

Ever married;

Living with children;

Owning their own homes.

The only exception is college enrollment — the share of 30-year-olds with a bachelor's degree has nearly doubled since 1995.

So, is going to college worth it?

Milestone? Feels more like a neck-grinding millstone, doesn't it?!

Maybe yes, maybe no, but the "buyer's remorse" emotion seems to be hanging in the air.

You may also like

Kalshi early employees: Whoever controls the traffic controls the market

Tether signs contracts with four major audits, Circle's compliance moat collapses, stock price plummets by 20%

Proudly Introducing Aethir Claw: Your AI Agent, Our Infrastructure

Why Buying Gold Can Lead to Bankruptcy

If the US Treasury yield rises above 5%, will Bitcoin drop below $50,000?

Circle Plunges 20%: Crypto Earthquake Triggered by Draft Proposal

After the Smoke Clears: 5 Possible Endings to the Middle East Conflict

Stablecoin Yields Discontinued, Circle Plunges 20% in One Day

AI Wired into War Machine | Rewire News Nightly

Web3 is sick, but the cure is not AI

Why must Web3 projects be included in RootData?

Fluid Announces Updates on Resolv Hack Recovery and Compensation Plan

Key Takeaways Fluid has repaid approximately $70 million related to USR debts on the BNB and Plasma chains.…

Binance to Delist Key Spot Trading Pairs: What You Need to Know

Key Takeaways Binance is set to remove several spot trading pairs on March 27, 2026, at 11:00 AM…

Whale Activities in the Crypto Market: A Deep Dive into Recent Trends

Key Takeaways A significant whale deposit occurred 3 hours ago when 5.5 million USDT was moved to Binance…

Circle and Tether Freeze Iranian Exchange Wallex Wallet with $2.49M Assets on Hold

Key Takeaways Circle and Tether have frozen a significant amount of assets from an Iranian exchange called Wallex,…

James Wynn Engages in High-Leverage Bitcoin Short Position

Key Takeaways James Wynn recently opened a 40x leveraged short position on Bitcoin. His position involves 2.69 BTC,…

Major Whale Opens Significant 20x Leveraged Positions in ETH and BTC

Key Takeaways Whale 0x049b has executed large 20x leverage positions on 9,256 ETH and 282.47 BTC, totaling over…

New Whale Activity: 33,998 ETH Withdrawn from Kraken

Key Takeaways A new Ethereum whale with the address starting 0xD77 has withdrawn 33,998 ETH from Kraken. The…